Understanding LTV from a Business Perspective

Running a credit business is, at its core, running an interest-for-risk trade.

Acquisition costs money. Underwriting costs money. Collection costs money. Whether these investments pay off depends on whether customers are willing to borrow repeatedly and whether they repay on time. When a loan is issued, how much the business ultimately earns is not determined by how high the single-iteration interest income is—it is determined by how much net revenue the business can sustainably extract from that user before they churn.

This is the fundamental significance of LTV (Life Time Value) for the credit business: the total net revenue a business can generate from a user throughout their entire borrowing lifecycle, from first loan to final churn.

Why LTV Is Not Just a Risk Metric

Many assume LTV is the risk team’s responsibility—but in reality, LTV is the business owner’s responsibility.

The risk team asks: “Will this loan go bad?” That’s a risk question. But the business owner has a different question: “How much can I afford to spend acquiring this user without losing money?” These two questions are closely related but not identical.

For example, a user with a low risk score theoretically has a higher probability of default. However, if that user comes from a high-interest-rate product where the single-iteration interest income is substantial, even a 20% default rate might still result in a positive LTV. Conversely, a high-quality user with an excellent risk score from a low-interest-rate product might generate lower LTV.

LTV is the metric that combines risk and revenue into a single measure of success. It doesn’t answer “Is the risk model performing well?” It answers “Is this user worth acquiring?”

A One-Sentence Definition

LTV in the credit industry can be expressed with a simplified formula:

LTV = Σ(Periodic Interest Income − Periodic Bad Debt Loss − Periodic Operating Cost) × Duration

Where:

- Interest Income = Loan Amount × Interest Rate × Loan Term

- Bad Debt Loss = Loan Amount × Default Rate

- Operating Cost = Acquisition Cost + Underwriting Cost + Collection Cost

- Duration = Time from first loan to final user churn

This formula looks simple, but in practice every variable requires careful disaggregation. We will walk through each one in the sections that follow.

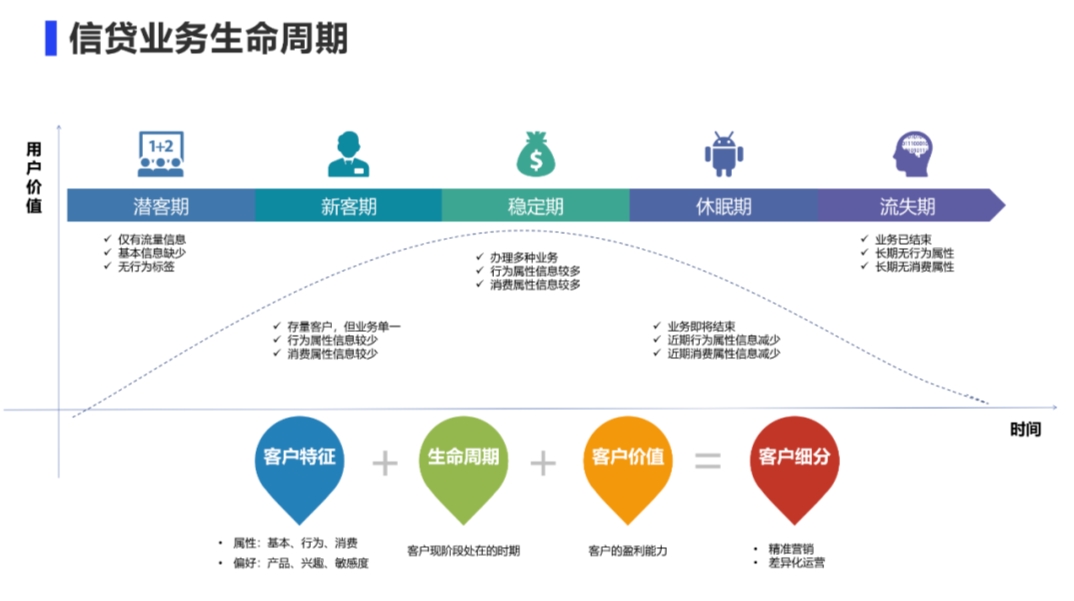

Three Lifecycle Stages of Credit Users

In the credit business, a user’s lifecycle can be divided into three core stages: Acquisition, Conversion, and Retention & Cycling. Each stage carries its own critical business questions and key performance indicators.

Acquisition: The Balance Between Channel and Quality

Acquisition is the starting point of the entire lifecycle—and the most expensive part.

In the digital credit landscape, the primary channels can be categorized as follows:

Facebook (Meta). This channel offers broad demographic coverage, with a relatively high proportion of users aged 25–45. These users tend to have more stable income and above-average willingness and ability to repay. However, CPA on Facebook has been rising steadily, making it increasingly difficult to achieve profitability relying solely on this channel in a competitive market.

Google. Search-intent users have clearer borrowing needs—someone who actively searches “loan” or “borrow money” is already showing strong borrowing intent. Google channels typically convert at higher rates than Facebook, but also carry higher CPA. A notable characteristic of Google-acquired users is a higher proportion of one-time applicants, meaning repeat-borrowing rates may not be optimal.

TikTok. The user base skews younger, with 18–30 year olds dominating. These users may have lower income stability but higher growth potential. TikTok CPA is typically the lowest among the three major platforms, but asset quality volatility is also higher, requiring more careful monitoring of early delinquency metrics.

Organic Traffic. Users arriving through app store searches or brand-name searches typically have basic product awareness and clear application intent. Their quality often exceeds paid channels, but the volume is limited and cannot serve as a primary acquisition source.

APK and Other Non-Paid Channels. Users acquired through APK installations, pre-installs, or offline promotions have heterogeneous quality and require channel-by-channel analysis. Some APK-acquired users may show signs of multi-borrowing, requiring special attention during underwriting.

The Core Logic of Channel Selection

The core business question is: At the current CPA level, can users from this channel generate enough interest income over their lifecycle to cover acquisition costs and turn profitable?

The answer is not static. For high-interest-rate cash loan products, tolerating a higher default rate is acceptable because single-iteration interest income is substantial. For lower-interest-rate consumer finance products, every unit of default is less tolerable, and channel quality requirements are higher accordingly.

This means that LTV-driven acquisition decisions are not about picking the cheapest channel or the highest-quality channel—they are about picking the channel with the highest overall return on investment.

In practice, we recommend tracking the following core metrics by channel:

- CPA (Cost Per Acquisition)

- First-loan conversion rate (proportion of approved applicants who actually receive funds)

- FPD7 (First Payment Default within 7 days of due date)

- M3 (Month-3 migration rate)

- 6-month repeat-borrowing rate

- Estimated composite LTV

Only by tracking this full set of indicators can you truly judge whether a channel deserves sustained investment.

Conversion: The Funnel from Application to Disbursement

A submitted application does not equal business revenue. From application to disbursement, two nodes in the conversion chain deserve particular attention.

Approval Rate: The First Funnel Gate

The approval rate is the first checkpoint in the conversion chain. The tightness or looseness of underwriting policy directly determines how many people enter the funnel and how good their quality is.

Loose underwriting — pros and cons: High approval rates mean large volumes of applicants converting to disbursed loans, and rapid business scaling. The trade-off is that incoming user quality is mixed, increasing future bad debt pressure. Especially when acquisition costs are high, if the default rate among admitted users is excessive, LTV turns negative and acquisition costs become pure overhead.

Tight underwriting — pros and cons: Bad debt pressure decreases and asset quality improves. But low approval rates waste substantial acquisition spend—money spent driving users in only to reject them at the underwriting stage. Meanwhile, business scale is constrained, and in a competitive market, this can mean losing ground to rivals.

There is no universally correct answer here. The key is finding the optimal balance for the current stage of the business:

- Rapid scaling phase: May need to accept higher defaults for volume, prioritizing user acquisition first

- Profitability pressure phase: Raise risk thresholds to ensure every disbursed loan generates positive returns

- New product launch phase: Use relatively strict policies first to establish stable asset quality data, then gradually relax

First-Loan Conversion Rate: The Last Hurdle Before Disbursement

It is very common in actual business for users to approve but never draw funds.

Common reasons for “approved but not disbursed” include:

Dissatisfactory credit limit. The limit granted by the system falls below the user’s expectations, and they deem the amount not worth borrowing. Common in products with conservative limit-setting logic.

Rate too high. Users see the displayed interest rate and find it unacceptable. This is especially pronounced among rate-sensitive segments (e.g., white-collar workers), where pricing slightly above their threshold causes churn.

Poor process experience. The application process is too long, requires too much documentation, and has a high mid-funnel drop-off rate. This is especially true for younger users acquired through TikTok and similar channels, who have higher expectations for process fluidity.

Insufficient lender capacity. In some periods, funding-side disbursement capacity is constrained, preventing some approved users from receiving funds on time. This is a supply-side constraint, not active user abandonment—it requires coordination between business and funding teams.

Improving first-loan conversion requires joint effort from business and risk teams:

- Limit design: Use income information, debt levels, and historical borrowing performance to design attractive initial limits while controlling risk

- Rate pricing: Find the user-acceptable price range based on risk cost + funding cost + operating cost + reasonable margin

- Process experience: Shorten the application flow, optimize identity verification, improve page load speed, and reduce mid-process abandonment

An empirical data point: every 5-percentage-point improvement in first-loan conversion rate can increase disbursement volume by 10–15% at the same acquisition cost. This leverage effect is substantial.

Retention & Cycling: Repeat Borrowing as an LTV Multiplier

A single loan generates one-time income. When users come back for a second or third loan, revenue compounds and LTV grows.

Repeat-borrowing rate is the metric that most amplifies LTV in the credit business—and also the one most easily overlooked in the early stages.

Many business teams over-focus on acquisition volume and first-loan conversion during product launch, neglecting the cultivation of repeat borrowers. By the time they realize 6 months later that the existing user base is shrinking and they have become dependent on constant new acquisition, LTV has already been eroded by high acquisition costs.

Characteristics of Repeat Borrowers

Users with high repeat-borrowing rates typically exhibit the following traits:

Good repayment history. Every historical loan was repaid on time with no delinquencies. This indicates the product is attractive to the user and their financial situation is relatively stable.

High credit limit utilization. Users who tend to max out their credit limit signal that the current limit may not meet their needs—there is room for limit increases.

Stable borrowing frequency. Users who apply for loans at regular intervals, forming habitual usage patterns.

After identifying high-repeat-borrowing users, the following approaches can further boost their LTV:

Credit Limit Management

After a period of use, the business system needs to decide whether to offer the user a credit limit increase.

Limit-increase decisions should consider multiple factors:

- Repayment history: Any delinquency records?

- Historical borrowing interval: Is the gap between loans stable?

- Application frequency: Is the frequency of loan applications increasing?

- Debt position: Has the user’s debt on other platforms increased?

Limit-increase strategies generally fall into two categories:

Proactive limit increases: Based on user behavior, the system actively raises the limit without user initiative. Suitable for users with strong credit records and high activity. This approach provides a better user experience but carries higher risk—if users quickly default after a limit increase, losses are larger.

Reactive limit increases: Users proactively apply for limit increases, and the business decides based on risk assessment. This approach is more risk-controllable but may deliver a poorer user experience (application rejection or small increase).

A reference cadence for limit increases: after 3 consecutive on-time repaid loans, consider a 10–20% increase; after 6 consecutive on-time repaid loans, further increase to 30–50%.

Cross-Selling

When a business has multiple product lines (e.g., cash loans, consumer loans, SME loans), it can recommend other products based on the user’s performance in existing products.

The value of cross-selling: a high-value existing user has a far lower conversion cost than a new user. The user already has brand awareness and product trust—no need to go through the full acquisition and underwriting process again.

However, cross-selling carries risk: if the recommended product is unsuitable and causes over-indebtedness, subsequent default losses may offset the cross-sell revenue. We recommend assessing the user’s comprehensive debt position before recommending additional products.

Four Key Business Metrics

With the LTV framework understood, the next step is to identify which metrics deserve the most day-to-day attention. These four metrics form the credit business foundation.

CPA vs. LTV Balance

CPA (Cost Per Acquisition) is a direct measure of acquisition efficiency. But CPA alone is just a cost number—meaningless without LTV context.

The correct evaluation framework is: LTV > CPA + Operating Cost + Funding Cost, or the business cannot sustain itself.

This inequality looks simple, but in practice many business teams have never carefully verified the actual values on the right side. Operating costs and funding costs are relatively fixed, but CPA and LTV are both variables—and they are often correlated. Lower-CPA channels may have inferior user quality, resulting in lower LTV; higher-CPA channels may have better user quality, supporting higher LTV.

LTV differences across channels can be substantial. Consider this illustrative data:

| Channel | CPA | 3-Month LTV Est. | 6-Month LTV Est. | LTV/CPA (6-Month) |

|---|---|---|---|---|

| 18 CNY | 45 CNY | 72 CNY | 4.0 | |

| 22 CNY | 52 CNY | 80 CNY | 3.6 | |

| TikTok | 12 CNY | 22 CNY | 31 CNY | 2.6 |

| Organic | 0 CNY | 20 CNY | 28 CNY | ∞ |

Several key observations from this data:

First, TikTok has the lowest CPA but also the lowest LTV, indicating this channel’s user quality is inferior or product-market fit is poor—one cannot judge a channel as good simply because its CPA is low.

Second, Facebook and Google have higher CPA but stronger LTV performance, making them more suitable as primary acquisition channels.

Third, while Organic has zero CPA, its LTV is not outstanding; its main value lies in low-cost volume supplementation, and it is not suitable as the primary growth driver.

The essence of channel optimization is not finding the cheapest channel—it is finding the channel with the highest LTV/CPA ratio. However, this ratio alone is not the sole decision criterion; the business’s current cash flow situation and scaling ambitions must also be considered.

If the business is in a phase requiring rapid scale expansion, it may deliberately choose channels with lower LTV/CPA but also lower CPA (e.g., TikTok), trading profit for volume. If the business is under profitability pressure, it should prioritize channels with high LTV/CPA and reduce or pause investment in underperforming channels.

Default Rate: The Value of Early Risk Identification

Default rate is the most critical risk metric in the credit business—and the variable most directly impacting LTV. Defaults erode interest income and directly compress margins.

Default rates are measured through multiple lenses:

FPD (First Payment Default). When a user misses their first repayment due date, this is the earliest and most direct risk signal. FPD is typically used as an early warning indicator for channel quality and borrower segment quality.

M3/M6/M12 (Monthly Migration Rate). M3 represents what proportion of loans delinquent for 3 months migrate to more severe delinquency status. M3 is a core metric for asset quality stability. If M3 is significantly above industry average or historical comparables, asset quality is deteriorating.

Vintage Analysis. Grouping loans by their disbursement month (vintage) and tracking delinquency rates over time. Vintage analysis eliminates macro-economic interference and genuinely reflects differences in borrower quality across vintages and the effectiveness of risk policies.

Default rate analysis is not solely a risk team responsibility. Business leaders need to understand: current asset quality is the outcome of past decisions—which channel cohort, which pricing, which underwriting policy. Only by tracing this causal chain can better decisions be made going forward.

Specifically, default rate disaggregation can be conducted across the following dimensions:

By channel: What are the M3 rates for Facebook vs. TikTok users respectively? How large is the gap? Does this gap align with the CPA and LTV comparison?

By borrower segment: What are the default rates for new borrowers (first loan) vs. repeat borrowers? Does repeat-borrowing performance genuinely outperform new borrowers?

By product: Is asset quality consistent across cash loans and consumer loans? Can the interest rate pricing of different products cover corresponding risk costs?

By risk policy: When the same channel uses different risk rules at different times, does asset quality change noticeably?

The goal of default rate analysis is to identify “which dimensions have asset quality below expectations,” then analyze causes and adjust strategy. Looking only at a composite default rate number provides no actionable guidance.

Repeat-Borrowing Cycle: Time Is Money

Repeat-borrowing cycle refers to the interval between a user’s first disbursement and their second loan application. This metric matters because:

The shorter the repeat-borrowing interval, the more interest income a user generates within a fixed time period, and the faster LTV grows.

For example, two users each generate 100 CNY monthly interest. User A borrows a second loan within 30 days of their first; User B waits 90 days. After 6 months, User A has contributed 6 periods of interest income while User B has contributed only 2.

A short repeat-borrowing interval also indicates user satisfaction with the product experience and willingness to return. If a user disappears after one loan, this is not a normal lifecycle conclusion—it is churn. Possible reasons include poor product experience, insufficient credit limit, uncompetitive rates, or the user simply treating the first loan as a one-time emergency fund.

Tracking the distribution of repeat-borrowing cycles helps the business set rational user maintenance touchpoints. For example, if data shows 70% of repeat borrowers reapply within 30 days of their first loan maturing, pushing limit-increase or promotional messages during this window will significantly outperform random outreach.

Repeat-borrowing cycles also support user segmentation. Users with different cycle characteristics can be managed with different strategies:

Short-cycle users (interval <30 days): Highly active users indicating strong product stickiness. Can receive limit-increase incentives to further boost per-transaction loan amounts.

Medium-cycle users (interval 30–90 days): Normal repeat borrowers. Maintain status quo; consider proactive outreach near their previous loan maturity date.

Long-cycle users (interval >90 days): Low-activity users at churn risk. Deserve focused win-back efforts through targeted discounts, time-limited limit increases, or similar incentives.

Non-repeat users (no application record for 180+ days): Effectively churned. Reduce operational investment or attempt a final win-back before deprioritizing.

Average Loan Amount and Credit Limit

Average loan amount determines the base for single-transaction interest income. Higher averages theoretically generate more interest income, but excessively high averages may also increase user repayment pressure and elevate default rates.

Credit limit design must balance two objectives: letting users borrow an amount that meets their needs (demand side), while keeping that amount within their repayment capacity (risk side).

A reference framework for limit design:

First-loan limit. For new borrowers, the initial limit should not be excessive. A reasonable guideline is to cap it at 30–50% of the user’s monthly income (where income verification is available). Exceeding this ratio significantly increases repayment pressure and subsequent delinquency risk. For scenarios without income verification, other data points (social behavior, device information, historical credit records) must supplement the assessment.

Repeat-loan limit. As users continue using the product and repay on time, limits can be gradually increased. Users with strong performance have greater limit upside—which is a lever the business uses to increase LTV. Hard caps on increases must be set to prevent user over-leveraging.

Aggregate limit management. In multi-product businesses, the combined debt position across all products must be monitored. If a user already carries significant debt in a cash loan product, recommending a consumer loan product requires caution.

There is also a trade-off between average loan amount and approval rate: higher amounts face stricter risk review, which lowers approval rates; lower amounts may achieve higher approval rates but generate less per-transaction interest income.

A practical strategy: provide new borrowers with relatively low initial limits (reducing risk pressure and boosting approval rates), then gradually increase limits as they demonstrate good repeat-borrowing behavior. This approach controls risk while using the repeat-borrowing stage to compensate for initially lower average loan amounts through limit increases.

Business Decision Scenarios

New Product Launch: Choosing the Target Segment

Before launching a new product, the most important decision is: Who is this product for?

The target segment determines credit limits, interest rate pricing, underwriting policies, and acquisition channels—every aspect of product design flows from this core choice.

High-Risk-Appetite Products

For high-risk-appetite products (higher interest rates, targeting lower credit-score segments), the business logic is using higher interest income to offset higher default losses.

Under this model:

- Pricing typically exceeds 100% annualized, sometimes much higher

- Target segments are users unserved by traditional financial institutions

- Underwriting policies are relatively loose, making up for quality with volume

- Acquisition channels may need to accept higher CPA

The key in this model is controlling loan amount and term—single-transaction amounts should not be too high, and loan terms should not be too long, ensuring that even if defaults occur, losses remain manageable. The core assumption of the LTV model is that users will borrow repeatedly, and after sufficient repeat cycles, total interest income will cover defaults and acquisition costs.

Low-Risk-Appetite Products

For conventional consumer finance products (lower interest rates, higher-quality target segments), the business logic is achieving profitability through lower risk costs and lower default rates.

Under this model:

- Pricing typically falls below 20% annualized

- Target segments are users with stable income (e.g., salaried workers, users with social insurance)

- Underwriting policies require stricter verification of income proof, social insurance contributions, and similar documentation

- Acquisition channels prioritize quality over volume

This model imposes higher requirements on acquisition cost and operational efficiency. LTV growth relies primarily on repeat-borrowing rates and user stickiness, not high interest income.

Recommended Path for New Product Launch

During the initial launch phase, we recommend testing 2–3 differentiated target segments with small samples and observing 3 months of actual asset performance before scaling.

Specific steps:

- Select 2–3 differentiated segments (e.g., first-tier city white-collar vs. third/fourth-tier city blue-collar; social insurance holders vs. non-holders)

- Disburse 500–1,000 loans per segment

- Track FPD, M3, and repeat-borrowing rates for 3 months

- Compare estimated LTV across segments and scale the best-performing direction

Do not scale blindly with insufficient data. Delinquency in credit products is lagging—assets that look fine in early stages may reveal their true quality problems 6 months later.

Channel Optimization: Where to Allocate Spend

Channel optimization is one of the areas most in need of LTV thinking in the credit business.

Whether to scale a channel cannot be determined by CPA alone—it depends on that channel’s LTV contribution.

Specifically, channel users can be segmented by monthly vintage; default rates and repeat-borrowing rates can be calculated by vintage cohort; and 3-month, 6-month, and 12-month LTV estimates can be projected and compared against CPA.

A practical channel evaluation framework:

Monthly Tracking Table:

| Channel | Monthly Disbursements | Monthly CPA | Monthly FPD | 3-Month M3 | 6-Month Repeat Rate | 6-Month LTV Est. |

|---|---|---|---|---|---|---|

| 5,000 | 18 CNY | 8% | 15% | 45% | 65 CNY | |

| 3,000 | 22 CNY | 6% | 12% | 50% | 72 CNY | |

| TikTok | 8,000 | 12 CNY | 12% | 22% | 30% | 31 CNY |

Based on this table, the following judgments can be made:

- Facebook and Google 6-month LTV is significantly higher than TikTok’s, and M3 is lower—priority should be given to scaling these channels

- TikTok has low CPA but poor asset quality and uncompetitive LTV—maintain current level or consider slight reduction

Channel optimization is not static. User quality fluctuates with seasons, competitive dynamics, and collection strategy changes. Holiday periods are typically peak demand seasons but may also carry elevated default risk. When competitors scale aggressively, your channel’s user quality may be diluted.

We recommend monthly reassessment of each channel’s LTV contribution and timely budget reallocation.

Existing User Operations: Who Deserves Priority Attention

Operating resources for existing users are limited. The core question is: Where should limited resources be concentrated?

Based on LTV contribution capacity, existing users can be categorized as follows:

High-Value Users

Users with good repayment history, stable borrowing frequency, and high credit limit utilization. These users are the core source of business profitability.

The operational goal for high-value users is extending their lifecycle and increasing repeat-borrowing frequency.

Specific tactics:

- Provide limit-increase incentives to grow per-transaction loan amounts

- Offer more competitive rate conditions to strengthen loyalty

- Provide dedicated customer service to elevate experience

- Prioritize new product recommendations (cross-selling)

High-value users have zero acquisition cost (they are already in the existing base), so the marginal return on operational investment is far higher than for new users.

Potential Users

Users whose historical performance is acceptable but whose recent activity has declined or borrowing intervals have lengthened. These users face churn risk and deserve focused attention and win-back efforts.

Recognition signals:

- Last borrowing was more than 45 days ago (exceeding the product’s average repeat interval)

- Credit limit utilization dropped from 80% to below 30%

- Click-through rate on push notifications has declined

Win-back tactics:

- Targeted discounts: Offer rates more competitive than those for new users

- Time-limited limit increases: Inform users their limit is about to increase, encouraging usage

- Churn surveys: Understand why users stopped borrowing and optimize accordingly

Low-Value Users

Users with poor historical performance, frequent delinquencies, or extremely low credit limit utilization. These users’ LTV contribution is marginal or negative.

The operational strategy for low-value users should be controlled investment with risk monitoring:

- No additional operational resources for win-back campaigns

- Continuous monitoring of repayment performance with timely collection triggering

- Maintain conservative credit limit management to avoid over-lending

Case Study

A cash loan product underwent a comprehensive review of its channel and user performance after 6 months of operation.

Channel-Level Data

Six-month channel performance data is as follows:

| Channel | Cumulative Disbursements | CPA | Avg. Loan Amt. | 6-Month Default Rate | 6-Month Repeat Rate | 6-Month LTV Est. |

|---|---|---|---|---|---|---|

| 32,000 loans | 18 CNY | 950 CNY | 14% | 48% | 68 CNY | |

| 18,000 loans | 22 CNY | 1,100 CNY | 11% | 52% | 76 CNY | |

| TikTok | 65,000 loans | 12 CNY | 720 CNY | 23% | 31% | 29 CNY |

| Organic | 8,000 loans | 0 CNY | 880 CNY | 16% | 42% | 34 CNY |

Conclusions:

- Facebook and Google channels both have LTV/CPA exceeding 3.0, making them the optimal channels—continuous scaling is recommended

- TikTok has the lowest CPA but LTV is only 29 CNY with LTV/CPA of 2.4 and a default rate as high as 23%—no additional investment is recommended

- Organic has zero CPA but unremarkable LTV; its main value is low-cost volume supplementation

User Segment Operations Data

The first month’s 10,000 disbursed users, segmented by their performance after 6 months:

| User Segment | Users | Share | Avg. Loans per User | Avg. Interest Contribution | Share of Interest Revenue |

|---|---|---|---|---|---|

| High-Value | 1,200 | 12% | 5.8 loans | 2,850 CNY | 42% |

| Potential | 2,300 | 23% | 2.4 loans | 980 CNY | 28% |

| Low-Value | 1,000 | 10% | 1.2 loans | 320 CNY | 4% |

| Churned | 5,500 | 55% | 1.0 loan | 470 CNY | 26% |

Key findings:

- 12% of high-value users contributed 42% of total interest revenue

- 55% of users never borrowed again after their first loan—these are typical “one-time users”

Business Decisions and Results

Based on the data, the business team implemented the following strategies:

Channel strategy: Increased monthly budgets for Facebook and Google by 30% each; TikTok maintained at current level with no additional investment.

High-value user limit-increase strategy: Progressive limit increases for the 1,200 high-value users. First increase: 20% after 3 consecutive on-time repaid loans; second increase: another 30% after 6 consecutive on-time repaid loans. After 6 months, this group’s average loan amount grew from 950 CNY to 1,480 CNY, with per-user interest contribution increasing approximately 65%.

Potential user win-back strategy: Targeted discount offers (first-period rate at 20% off) sent to 2,300 potential users. Win-back cost was approximately 45 CNY per user. The 3-month LTV contribution from recalled users averaged 180 CNY, achieving an ROI of approximately 4x.

Churned user strategy: No active win-back efforts for the 5,500 churned users; included only in unified promotions when new-user campaigns were launched.

Six-month performance comparison:

| Metric | Before (Month 1) | After (Month 6) |

|---|---|---|

| Overall Repeat Rate | 35% | 48% |

| High-Value User Share | 12% | 18% |

| Overall LTV/CPA | 2.8 | 3.6 |

Operational Implementation Recommendations

First Steps to Building LTV Thinking

LTV is not built in a day. We recommend starting with the following steps:

Step 1: Data Infrastructure.

Connect end-to-end data across acquisition, approval, disbursement, repayment, and collection—ensuring every user’s lifecycle events can be tracked and attributed.

Specifically, the following data challenges must be addressed:

- Channel attribution: Every disbursed user can be traced to a specific channel and ad campaign

- Unique user identification: A user’s borrowing records across different time periods can be linked to the same individual

- Cost accounting: Acquisition, underwriting, and collection costs can be allocated to specific users or orders

Data infrastructure is the foundation of all subsequent analysis. If data is inaccurate, LTV is built on sand.

Step 2: Define Methodology.

Clarify the LTV calculation methodology. Different business models may use different LTV definitions:

- Should funding cost be included? Is funding cost calculated using internal funds transfer pricing (FTP) or actual financing rates?

- Should operating cost be included? Is operating cost allocated per head or per order?

- Is default provision calculated using actual losses or expected losses (EL)?

Without consistent methodology, data is incomparable. Business, risk, and finance teams must align on methodology before analysis begins.

Step 3: Establish Regular Review Cadence.

We recommend monthly reviews, with LTV and its component variables (default rate, repeat-borrowing rate, average loan amount) disaggregated by channel, segment, and product.

Core questions each review meeting should answer:

- Did each channel’s LTV meet targets this month?

- Did any channel show a significant LTV decline? What caused it?

- Is reallocation of channel budget necessary?

Common Business Misconceptions

Misconception 1: Focusing on acquisition volume while ignoring acquisition quality.

Scale expansion masking bad debt problems is the most common fatal path in the credit business.

The typical pattern: a business leader sees new user numbers growing month after month and feels the business is thriving. Upon closer inspection, however, new-user default rates are climbing and repeat-borrowing rates are declining—the LTV has already turned negative. Growth is only occurring because acquisition costs are sufficiently low, not because the business is actually healthy.

Misconception 2: Treating first-loan revenue as final LTV.

Single-transaction interest income cannot cover acquisition costs—only repeat borrowing can truly generate profit.

Many products design pricing strategy based solely on whether single-iteration loan interest can cover funding costs and risk costs, ignoring repeat borrowing entirely. If this assumption holds, the business’s core strategy becomes constantly acquiring new users—but as market acquisition costs continue rising, this path eventually becomes unsustainable.

The correct mindset: treat the first loan as an acquisition tool, and repeat borrowing as the profit source. Only when users are willing to return for a second and third loan can LTV truly deliver positive returns.

Misconception 3: Treating LTV as a risk team responsibility.

LTV thinking is an essential framework for business leaders. Risk provides data and model support, but business decisions must be made—and owned—by the business leader.

If a business leader doesn’t understand LTV, they lose their decision-making compass across every aspect of operations: Should a channel be scaled or cut? Should a user receive a limit increase or not? Should the product’s price be reduced or increased? All of these questions can be answered through the LTV lens.

Misconception 4: Ignoring the impact of collection on LTV.

When defaults occur, collection efforts can recover some losses. But collection itself has costs, and collection efficiency declines as accounts age.

More critically, collection methodology affects future user behavior. If collection methods are too aggressive (e.g., exposing contact lists, excessive harassment), users may permanently churn—even if they eventually repay, they will never borrow again. Collection strategy must balance “recovery rate” against “user relationship maintenance.”

How to Work with Risk and Product Teams

LTV implementation requires cross-functional collaboration—no single team can do it alone.

Risk team provides:

- User credit scores, default rate predictions, and collection efficiency data

- Simulation of how risk policy changes impact LTV

- Risk assessments for limit and pricing strategies

Product team is responsible for:

- Continuous optimization of borrowing experience, limit display, and process pages

- Improving first-loan conversion and process flow

- End-user product design and interaction optimization

Business/Operations team is responsible for:

- Developing channel strategy and user operation strategy based on LTV data

- Coordinating risk and product resource prioritization

- Owning end-to-end business results

If these three functions operate in silos, the LTV system cannot truly land. Common failure modes: the risk team says “my risk model is excellent and default rates are well-controlled,” but the business team says “approval rates are too low and users can’t get in”; the product team says “the borrowing flow is already very smooth,” but repeat-borrowing data shows users are not coming back.

The key is establishing shared metric language and a common business objective—maximizing user lifetime value within controlled default boundaries.

One recommended practice: hold monthly LTV review meetings with risk, product, and business teams together, using the same dataset to evaluate performance and decide next actions. This prevents the fragmentation and finger-pointing that occurs when teams operate in isolation.

Closing Thoughts

Understanding LTV is not the destination—it is the starting point.

The credit business is fundamentally a combination of risk pricing and user management. LTV provides the unified metric for judging whether both are being done well. In actual business operations, the most important ongoing work for any business leader is continuously tracking, dissecting, and optimizing LTV.

A few final takeaways:

First, LTV thinking is not about reading numbers—it is about making decisions. Knowing a channel’s LTV is step one. Deciding whether and how to scale based on that number is where LTV thinking actually delivers value.

Second, data quality determines the ceiling of your analysis. If channel attribution is inaccurate, users cannot be identified across periods, and cost allocation is unclear, LTV calculations will be distorted and business decisions will be wrong. Build the data foundation first.

Third, cross-functional alignment is the key to LTV implementation. If risk, product, and business are not working from the same definitions and toward the same goals, the LTV system becomes each team’s own isolated data exercise.

We hope this article provides an actionable framework for your business. If you have specific implementation questions, we welcome further discussion.